Market News

Canada’s Economy Rests Between Roars - SCOTIABANK

- Canada’s economy is experiencing a mild, transitory setback…

- ...as the economy roared a little softer than guided in Q1…

- ...but ended Q1 with a powerful burst of activity…

- ...and temporarily stumbled into Q2 due to lockdowns

- Q2 GDP is likely to end stronger after April–May weakness…

- ...and set up potentially powerful growth into Q3

- Markets largely ignored it all…

- ...and so should policy makers in favour of smoothing Q2–Q3

Canadian GDP Q1, q/q SAAR:

Actual: 5.6

Scotia: 6.6

Consensus: 6.8

Prior: 9.3 (revised from 9.6)

Canadian GDP March, m/m % SA: 1.1

Canadian GDP April, m/m % SA, flash: -0.8

Canada’s economy roared by a little less than previously indicated in Q1 but stumbled into Q2 which is only somewhat surprising given that much of the economy was in lockdown with stay at home orders throughout the month. I say ‘somewhat’ because prior bouts of tighter restrictions have nevertheless been marked by steady growth in the size of the economy month after month through the second wave. The gig was up in April and May is unlikely to be any better before a sustained expansion is expected to return starting in June.

The economy grew a little slower during Q1 but exited the quarter a little faster in March than Statistics Canada had previously guided based upon earlier partial evidence. With fuller evidence the agency says the economy expanded by 1.1% m/m in March (instead of the ‘flash’ estimate of 0.9%) and by 5.6% q/q annualized in Q1 overall (instead of the ‘flash’ estimate of 6.6%. Further, the torrid pace of growth in Q4 was revised a little softer at 9.3% (from 9.6%).

That’s all history now of course and so on the back of what are still two resoundingly strong quarters for growth over Q4-Q1 we’re now left with a set back in Q2. Preliminary guidance for April GDP indicates a 0.8% m/m drop. Yes drop. We haven’t seen a drop at all since way back in April of last year but bear in mind that one was a doozy (-11.2%).

What this means is that Q2 GDP is tracking flat so far. Ok, 0.2% q/q annualized to be technically correct and by taking April as representative of the quarter over the Q1 monthly GDP average (chart 1). That’s not to say we know what May and June will be; rather, it’s to keep the tracking math free and clean of any arbitrary imposition growth assumptions when we obviously don’t have any data for May or June as of yet.

My hunch is that the quarter is going to end much stronger than the way in which it began such that after weak months in April and May, June GDP could bounce higher and represent a nice exit point into Q3 GDP. That’s a fancy way of guiding that policy and markets should look through the April–May noise not as narrative busting but as a deferral of activity into subsequent months. The best advice at this point is to look through both Q2 weakness and a likely Q3 bounceback and smooth the two. That would treat the noisy data along the path as just an intertemporal distribution of activity from one quarter to the next which fuss trained eyes and ears. Data will inform tracking of this view.

The economy ended April about 1.9% smaller than it was just before the pandemic struck dating back to February 2020 (chart 2). That’s still notable, but it’s a far cry from the 17.6% contraction over the February 2020 to April 2020 period after which the recovery began to set in.

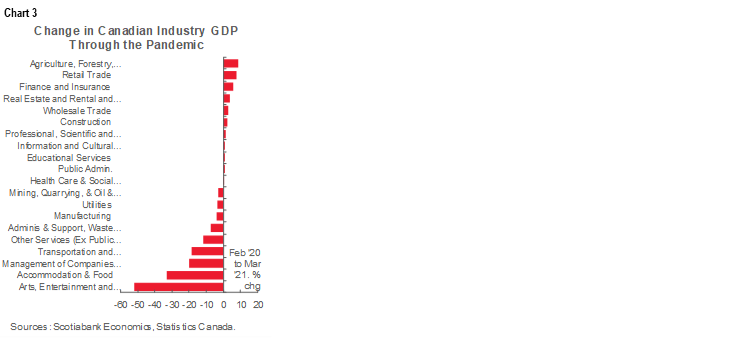

Chart 3 shows the cumulative change in GDP by sector of the Canadian economy since the pandemic set in. Some sectors are still mildly in the black with most of the pain still focused upon a handful of sectors and notably accommodation and food services (hotels, restaurants, bars etc) and arts and entertainment related activities.

As for details behind the Q1 quarterly GDP reading, chart 4 shows the weighted contributions to growth by driver, including consumption, investment, inventories, government spending and net exports. Consumption and housing investment did most of the work with a modest contribution from exports offset by greater import leakage as inventory depletion was a drag on growth. Business investment was a flat contributor.

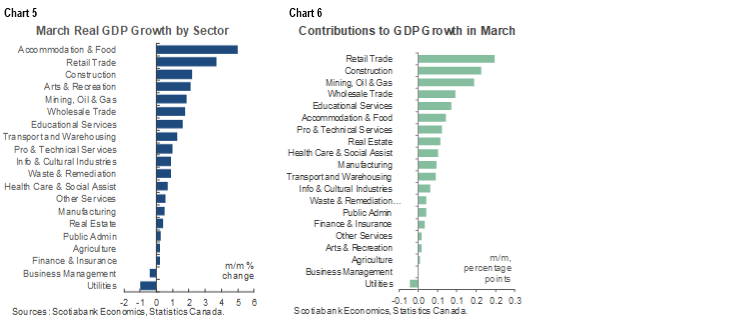

As for details behind the monthly GDP readings, we only have them for March with chart 5 showing monthly GDP changes by sector and chart 6 showing weighted contributions to growth. March was not only a strong one for overall growth but the breadth of industries that participated in the expansion before lockdowns was pretty impressive. All we know for April is that Statistics Canada loosely guided that it wasn’t just socially distanced sectors like retail trade and the accommodation and food services sectors that were weak, but also manufacturing, real estate and rental/leasing activities plus education. I’d ignored the guidance on the education sector because it’s probably a messed up seasonals thing given that Ontario delayed its March break for schools into April so the education sector’s activity was abnormally impaired last month (and artificially buoyed by 1.6% in March given the absence of the usual break). We’ll have to see whether the softness in manufacturing and real estate was also just a function of restrictions which is what I think given stay at home orders, banned open houses etc.